The Merged R&D tax relief scheme was brought in for accounting periods starting on or after 1st April 2024, the vast majority of which will have ended on or after 31st March 2025. What this means is that, as of 31st March 2026, we’ve had a full year of claims being submitted under the new rules.

Here at WhisperClaims, we saw this anniversary as an excellent time to do a deep dive into the claims prepared by our users and see what the profile of claims made under the merged scheme look like, and how they compare to claims made before the new rules came into force.

This second blog (you can read part 1 here) looks at claims prepared over the past four years, to explore how adviser behaviour and claim characteristics have changed through a period of significant legislative and compliance change. We’ll examine how both claim year and submission year affect the claims, including how long they took, what sectors they related to and how they were distributed geographically.

This analysis pulls together data from over 2500 claims prepared using WhisperClaims, from April 2022 to March 2026. These were split into groups based on both claim periods, to show the effect of legislative changes tied to specific accounting periods, and preparation date, and to show the effect of universal legislative changes, such as the introduction of the Additional Information Form (AIF), as well as the impact of HMRC’s compliance activities.

Some, but not all claims, had all of the required data, so where data, such as SIC code, was missing these claims were excluded from the relevant analyses. No other normalisation or data manipulation was carried out.

As might be expected from the time period in question, the vast majority (84%) of claims were SME scheme claims. The remainder were 3% old RDEC, 6% mixed SME/old RDEC, 2% ERIS and 5% new RDEC.

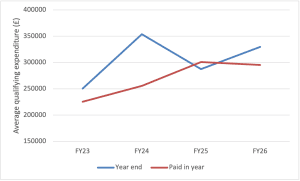

The average qualifying expenditure across all claims prepared during the time period was just under £270k, which aligns with HMRCs published figures. There was some variation across each year, and between claims prepared in the year vs claims for the accounting period, as shown in Figure 1.

Figure 1: Average QE (£) for claims prepared in each year and claims with a year-end within the year.

Both groups show a general increase in average QE over time, suggesting a shift towards larger claims being prepared within the dataset. The year-end analysis does show a slight reduction in average QE for claims ending within the FY26 financial year, which could show a delay in larger claims being submitted due to the additional complexity of preparing merged scheme claims.

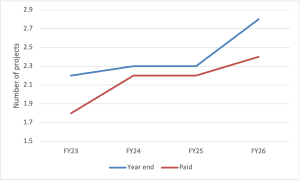

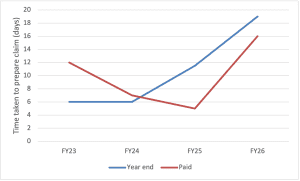

The average number of projects included in a claim increased from 2.1 for pre-merged scheme claims to 2.7 for merged claims, and the median time taken to prepare a claim increased from seven days for pre-merged scheme claims to thirteen days for merged scheme claims. This is perhaps unsurprising given the additional complexity introduced by the merged scheme, alongside the learning curve associated with a significant change in legislation. Taken together with the QE data, these findings suggest that claims prepared under the merged scheme may require more time and supporting detail than their predecessors. They may also indicate that smaller claims are becoming less prevalent within the dataset, although the reasons for this are difficult to determine from the data alone.

When we look at this data across the past four years, grouped as before by claims paid for (proxy for submission date) or financial year end, an interesting picture emerges, as shown in Figures 2 and 3.

Figure 2: Average number of projects per claim prepared in each year or with a year end in each year

Figure 3: Median time taken to prepare a claim for claims prepared or with a year end in the financial year

In both groups, the number of projects included has increased markedly over time, indicating that claimants and advisers have reacted to the changes, especially the introduction of the AIF, by including more detail in claims.

Figure 3 shows that the time taken to prepare a claim reduced between 2023 and 2025, which likely reflects growing familiarity with the AIF and the associated preparation process. The introduction of the merged scheme has likely caused this to shoot up again as claimants and advisers grapple with the new rules and requirements. It will be interesting to see whether this trend repeats itself over the coming years as advisers become more familiar with the merged scheme.

The sector distribution for pre-merged and merged scheme claims was broadly similar, with the top four sectors being construction, professional, science and technical, manufacturing and telecommunications, as would be expected from HMRC’s statistics. There were no significant shifts in distribution between the two groups of claims, demonstrating that the pool of companies applying for R&D tax relief has remained broadly similar.

When the data was analysed by year of claim preparation, the results were broadly similar – there were no significant shifts between sectors, despite HMRC’s campaigns and targeting of claims for companies in less technical sectors. However, there were very few claims prepared using WhisperClaims for companies in less technical sectors, so this might reflect more on the habits of WhisperClaims customers rather than the sector as a whole.

Taking all claims together, the geographical distribution was broadly consistent with previous statistics. The top locations were London and the South East, although there was a higher than expected number of claims in Scotland, probably due to WhisperClaims itself being based in Edinburgh. There was also little difference in sector distribution over time.

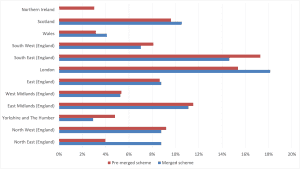

Separating out the merged and pre-merged claims threw up a few small differences, as shown in Figure 4.

Figure 4: Geographical distribution of pre-merged and merged scheme claims

No claims under the new rules were prepared for Northern Irish companies during the periods analysed. Given the introduction of NI ERIS and the distinct rules that apply, the absence of Northern Ireland claims is an interesting finding. However, with no claims in the dataset it is difficult to draw firm conclusions. It may reflect the relatively small sample size, lower levels of adviser activity in Northern Ireland, or uncertainty surrounding the NI ERIS rules following the delayed publication of legislation and guidance.

There were increases in claims made under the merged scheme in London and the North East. Given the relatively small number of claims involved, these differences may simply reflect normal variation within the dataset.

Overall, the data suggests that the profile of claims being prepared under the merged scheme remains broadly similar to those prepared under the previous rules. Average qualifying expenditure, sector distribution and geographical spread all show more continuity than change. This is perhaps unsurprising given that the merged scheme changes how relief is calculated and claimed rather than fundamentally changing the types of businesses carrying out qualifying R&D.

Where the most noticeable differences emerge is in how claims are being prepared.

Over the past four years, the number of projects included within claims has increased, while the time taken to prepare a claim has also risen. Although it is difficult to attribute these changes to any single factor, they are consistent with a more structured and evidence-based approach to claim preparation. The introduction of the AIF, increased HMRC scrutiny and the arrival of the merged scheme have all required advisers to adapt their processes and spend more time understanding and documenting claims.

Perhaps the most interesting finding is that while the companies claiming relief appear broadly similar to those seen before the legislative changes, adviser behaviour appears to have changed significantly. The data suggests that firms are investing more time in claim preparation and providing more detailed supporting information than was typically the case a few years ago.

For advisers, this reinforces the importance of having robust processes around project identification, evidence gathering and scheme selection. Firms that can apply those processes consistently are likely to be better placed than those relying on outdated assumptions or informal approaches.

As with any dataset of this size, care should be taken not to overstate the findings. However, the trends observed provide an interesting snapshot of how advisers and claimants have responded to one of the most significant periods of change the R&D tax relief regime has experienced.

On Wednesday 10 June at 12 noon, we’ll be exploring these trends in more detail, including what they may reveal about adviser confidence, scheme selection behaviour, regional variation and how firms are adapting their R&D tax processes. We’d love you to join us!

Subscribe to email updates

© 2026 Wobbegong Technology Ltd (Registered number 10754811), trading as WhisperClaims.

WhisperClaims is a registered trademark of Wobbegong Technology Ltd (Trade Mark No.: UK00003360482).