The Merged R&D tax relief scheme was brought in for accounting periods starting on or after 1st April 2024, the vast majority of which will have ended on or after 31st March 2025. What this means is that, as of 31st March 2026, we’ve had a full year of claims being submitted under the new rules.

Here at WhisperClaims, we saw this anniversary as an excellent time to do a deep dive into the claims prepared by our users and see what the profile of claims made under the merged scheme looks like, and how they compare to claims made before the new rules came into force.

This first blog will look at the overall merged scheme claim profile, including how long they take, what sectors they relate to and how they are distributed geographically. A follow-up blog will cover how these differ from claims made under the old rules.

As of 31st March 2026, 171 merged scheme claims had been prepared using the WhisperClaims app by 43 different advisory firms and accountancy practices. No claims were excluded and no data normalisation was carried out.

As might be expected from the stringent ERIS criteria, most claims fell under the new RDEC rules, with just 23% of claims qualifying for ERIS and the remaining 77% falling under RDEC.

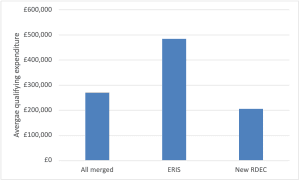

The average QE across all merged scheme projects was just over £270k, similar to what we’ve seen in pre-merged scheme claims.

Figure 1: average QE across all merged scheme, ERIS and RDEC claims

However, as shown in Figure 1, there was a large disparity between the average QE of ERIS and new RDEC claims, with the average QE of ERIS claims 137% higher than that of new RDEC claims.

This difference could be due to the smaller number of ERIS claims skewing the data, but further analysis of the numbers suggests that this is a true difference, and is more likely to be due to higher R&D intensities in ERIS claimants, as would be expected.

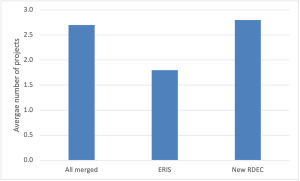

The average number of detailed project write-ups across all merged scheme claims was 2.7, suggesting that most claimant companies carry out a few projects per year and are required to include all of them in the Additional Information Form.

Figure 2: Average number of projects across all merged scheme, ERIS and RDEC claims

As shown in Figure 2, the average number of projects included in an ERIS claim was significantly lower than in RDEC claims, at 1.8 and 2.8 respectively.

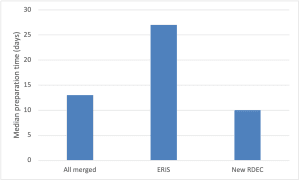

To take this a step further, we looked at the time taken from claim creation to claim finalisation in the WhisperClaims app as a measure of how long merged scheme claims took to prepare.

Figure 3: Median time (days) from claim creation to finalisation for merged, ERIS and RDEC scheme claims

Unexpectedly, Figure 3 shows that ERIS claims take over two weeks longer to prepare than RDEC claims, even though the average number of projects is lower. Taken alongside the data about qualifying expenditure, a picture begins to emerge of ERIS claims being made by smaller companies carrying out a very small number of highly complex and expensive R&D projects.

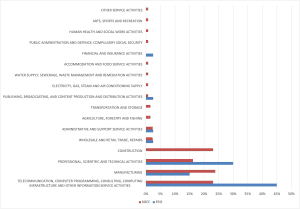

The sector distribution for merged scheme claims was very similar to what would be expected from previous years’ HMRC statistics, with the top four sectors being construction, professional, science and technical, manufacturing and telecommunications.

However, when the claims are split into ERIS and RDEC claims, there are some stark differences in sector distribution, as shown in Figure 4.

Figure 4: Sector distribution of ERIS and RDEC claims

This shows disparities in all four most common sectors, with all construction claims and significantly more manufacturing claims being claimed through the RDEC scheme, and significantly more professional, scientific and technical and telecommunications claims qualifying for ERIS.

This may suggest that ERIS claims are currently concentrated in sectors where technical activity and R&D intensity are easier to evidence or more confidently identified by advisers.

Taking all merged scheme claims as a whole, the geographical distribution was broadly consistent with previous statistics. The top locations were London and the South East, although there was a higher than expected number of claims in Scotland, probably due to WhisperClaims itself being based in Edinburgh.

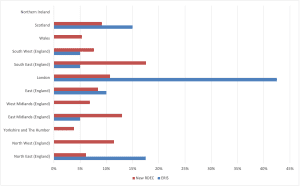

However, as with the sector distribution, there are some significant differences in geographical distribution of claims when ERIS and RDEC claim data is separated, as shown in Figure 5.

Figure 5: Geographical distribution of ERIS and RDEC claims

Most ERIS claims were made for companies in London or the Northeast, whereas RDEC claims were more concentrated in the Southeast and Northeast. In addition, there were several areas, including Wales, the West Midlands, Yorkshire and the Humber and the North West where all prepared claims were through the RDEC scheme. No claims for Northern Irish companies were prepared during the period analysed.

Overall, the main observations from the data are that, as expected, ERIS claims are being made by companies who are carrying out one or two highly complex projects in technical sectors and geographical areas where these technical companies are more concentrated.

However, the data does also suggest that, in some cases, companies that could claim through ERIS are not, possibly due to the complexity of the process and inexperience on the part of advisers. It seems unlikely, for example, that no Welsh companies meet the ERIS criteria, so there’s a chance that these claims are being routed through RDEC, as advisers seek to reduce the risk of claiming R&D tax relief.

Regarding the absence of claims from Northern Ireland, given the introduction of the NI ERIS scheme and the distinct rules that apply, this is an interesting finding. However, with no claims in the dataset, it is difficult to draw any firm conclusions. It may reflect the relatively small sample size, lower levels of adviser activity in Northern Ireland or uncertainty surrounding the NI ERIS rules following the delayed publication of legislation and guidance. This uncertainty may have undermined adviser confidence in preparing these claims.

The key thing that this data highlights for advisers is the need to identify quickly and accurately which scheme the claim is likely to qualify for, as this will affect how the claim is prepared, the amount of information required, and the time needed to pull it together. Additionally, it’s important to guard against bias, for example assuming that a construction company will definitely claim RDEC, and make sure that you understand the rules of the new schemes, especially NI ERIS, well enough to give robust and accurate advice to your clients.

In our upcoming webinar, we’ll explore these patterns in more detail including what they may reveal about adviser confidence, scheme selection behaviour, regional variation and how firms are adapting their R&D processes under the merged scheme.

Subscribe to email updates

© 2026 Wobbegong Technology Ltd (Registered number 10754811), trading as WhisperClaims.

WhisperClaims is a registered trademark of Wobbegong Technology Ltd (Trade Mark No.: UK00003360482).